If there is true information on your report that is bad for you, credit bureaus can usually only report for 7 years. They can report bankruptcy information for 10 years.

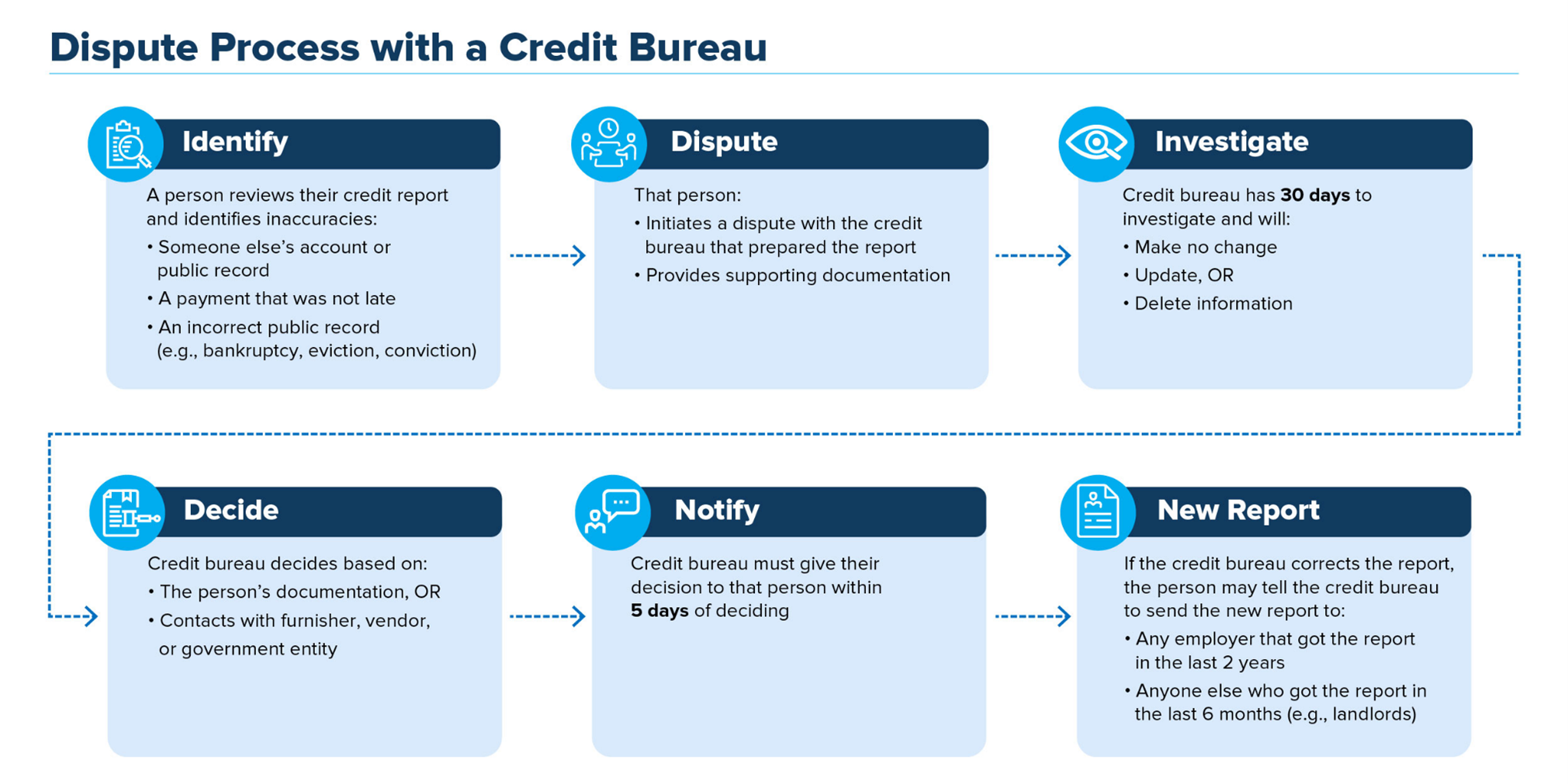

If something is not true is on your credit report, you should contact the credit bureau(s) that list the mistake(s) and the business(es) it is listed for. The page here tells how to do it. Here's how. Contacting them to say that the report is wrong is called a “dispute”.

After you contact them to say it is wrong, credit bureau(s) must check what you question within 30 days, unless they decide that your dispute is frivolous. If they find it frivolous, they must give you a reason. Sometimes this may be that you need to give them more evidence. The credit bureau(s) will forward your evidence to the business(es) that gave the information. The business(es) then must check and report back to the credit bureau(s).

If the credit bureau agrees with you after these steps your dispute is called “resolved”. If this happens, the credit bureau must tell you in writing and give you a free credit report. This does not count as your free annual report.

You can also ask that the credit bureau send notices of the correction(s) to anyone who got your report in the past six months and to anyone who got a copy for job purposes during the past two years. If you ask, the credit bureau must send the updated reports.

If the credit bureau does not agree with you after it checks, you can ask that your credit reports say that you disagree with the information. (This is called a “statement of dispute”). Also, you can ask that the credit bureau give your statement to anyone who got a copy of your report recently, but you can be charged a fee for this.

You can ask within 60 days of when someone denies you credit, a rental, insurance, a jog, or hurts you in some other way because of your credit report and can get another free credit report. The company must send you a notice that includes the name, address, and phone number of the credit bureau that they used You request the free credit report from that credit bureau.

You are also entitled to another free report each year if:

You may be thinking about hiring a company to help investigate mistakes on your credit report and to “repair” your credit. But anything a credit repair company can legally do, you can do for yourself at little or no cost. If you hire a credit repair company, it is important to know your rights.

It is illegal for credit repair company to charge you before they help you. It is illegal for credit repair companies to lie about what they can do for you. Credit repair companies also must explain:

If you choose not to hire a credit repair company, you can rebuild your credit by:

If you are in debt and need help, you might get help from a reputable credit counseling organization. For a list of approved credit counseling agencies, click here.

You are dealing with a credit repair scam if a company:

If a company promises to create a new credit identity or hide your bad credit history or bankruptcy, it’s a scam. These companies often use stolen Social Security numbers or get people to apply for Employer Identifications Numbers from the IRS under false pretenses to create new credit reports. If you use a number other than your own to apply for credit, you won’t get it, and you could face fines or prison.

If you have a problem with a credit repair company, report it to:

MLMs and Ponzi/pyramid schemes often seem similar, however there are minor differences that distinguish them.

Pyramid schemes usually promise large profits primarily mainly from recruiting others to join the “program”. Profits are not based on any real investment or sale of goods. Recruits are often encouraged to buy more products to sell than they could ever sell. They may be few actual sales.

A Ponzi scheme is very similar to a pyramid scheme, however in a Ponzi scheme there is no product. Ponzi schemes are often called “Peter-Paul” scams because there is no real investment opportunity. The promoter uses money from new recruits to pay the benefits promised to earlier recruits. Promoters in Ponzi schemes will often use high-pressure sales tactics to get you to join. They may emphasize that you will lose the opportunity if you don’t act quickly.

In Multi Level Marketing (MLM), companies sell their products or services through person-to-person sales. Sellers also bring in new sellers. When a new seller sells something, those higher up the chain gets a cut.

A MLM will not require you to recruit others to be paid.

Researching the company, researching what others are saying, considering the products the company offers, understanding the costs of joining, asking about refunds, and reading the paperwork can all help avoid schemes.

If you have information of a possible Ponzi or pyramid scheme, or if you have fallen victim to either of the schemes, you can file a tip to the SEC here. You can also leave a tip by phone with the FBI at 1-800-225-5324.

The IRS offers some relief to victims of these schemes through special tax rules. Investors in Ponzi schemes are entitled to deduct their losses as a theft loss, an itemized deduction, during the year the fraud is discovered.

You should also contact your local police department and file a complaint.

For more information visit the Consumer Information page on the FTC website.